Chandana Patnaik

In 2014, Toyota opened the doors to the hydrogen society by launching Toyota Mirai, the world’s first commercial FCEV (Fuel Cell Electric Vehicle). However, Mirai was not the first FCEV developed in the world. The credit of introducing the first FCEV to the world goes to General Motors, which developed Electrovan more than a half century ago in 1966.

The GM Electrovan containing 2 giant storage tanks forhydrogen and oxygen, 32 fuel cell modules, electric motor, and a 550-feet piping throughout the rear of the vehicle weighted around 7,100 pounds. This system relied on rare metals including platinum, which made it too expensive, and no proper hydrogen infrastructure was there those days, which made this vehicle a failure.

From GM Electrovan, that had a range of just 160 Kms, to today’s fuel cell vehicles that can range easily more than 600 Kms, the new-age fuel cell vehicles have seen a transition of innovation.

An era of risky storage, prohibitive cost, and with less room has ended with the dawn of high-pressure vessels, specifically – Carbon Composite Hydrogen Tanks (CCHTs) for fuel storage.

Carbon Composite Hydrogen Tanks, Their Types, & Applications

CCHTs are the pressure vessels fully wrapped by carbon composites with metallic or polymeric liners (Type III & Type IV). Type III tank has a metal liner (aluminium or steel) with full composite overwrap, whereas Type IV is a complete carbon fiber made tank having an inner liner made of polyamide or polyethylene plastic.

In 2021, hydrogen pressure vessels had nearly 7% share of the total pressure vessels market, a majority of which is

CCHT.

Table.1. Types of Pressure Vessels

The reason behind preferring carbon composites for the new-age hydrogen pressure vessels is that these materials are known for their superior strength & durability along with light weight, offering a mass-reduction between 50%-70%.

CCHTs find usage in a variety of applications, including cars, buses, trucks, forklifts, trains, ships, refuelling stations, bulk gas transportation, and back-up power. However, FCEV is the one application which generates over 90% of the demand for CCHTs.

FCEVs Fuelling the Demand of CCHTs

When it comes to hydrogen storage in FCEVs – it has been found that, to achieve long-range autonomy (over 500 kms), FCEVs must store 5-10 kgs of hydrogen safely, without adding much weight, in a compressed vessel at 700 bars. Here, type IV vessels take the lead in both value and quantity compared to type III tanks.

Notably, FCEVs including Honda Clarity, Hyundai Nexo, and Toyota Mirai employ compressed H2 at 700 bar pressure, featuring 2 or 3 type IV cylinders.

Specifications of a few FCEVs on road –

| FCEV Model | Fuel Tank Pressure | Driving Range Rating (miles) | Fuel Tank Capacity (Kgs) |

| Honda Clarity 2021 | 70 MPa/700 bar | 360 | 5.46 |

| Toyota Mirai | 70 MPa/700 bar | 402 | 5.6 |

| Mercedes-Benz GLC F-CELL | 70 MPa/700 bar | 478 | 4.4 |

In 2022, among the FCEV models, Hyundai Nexo recorded maximum sales of more than 11,000 units. The only major FCEV model behind Nexo was Toyota Mirai with an annual sale of more than 3,500 units in 2022.

As of 2022, there were >72,000 units of hydrogen fuel cell electric vehicles (FCEVs) globally. The count has increased by 40%, compared to 2021, according to the International Energy Agency’s (IEA) new Global EV Outlook 2023 report.

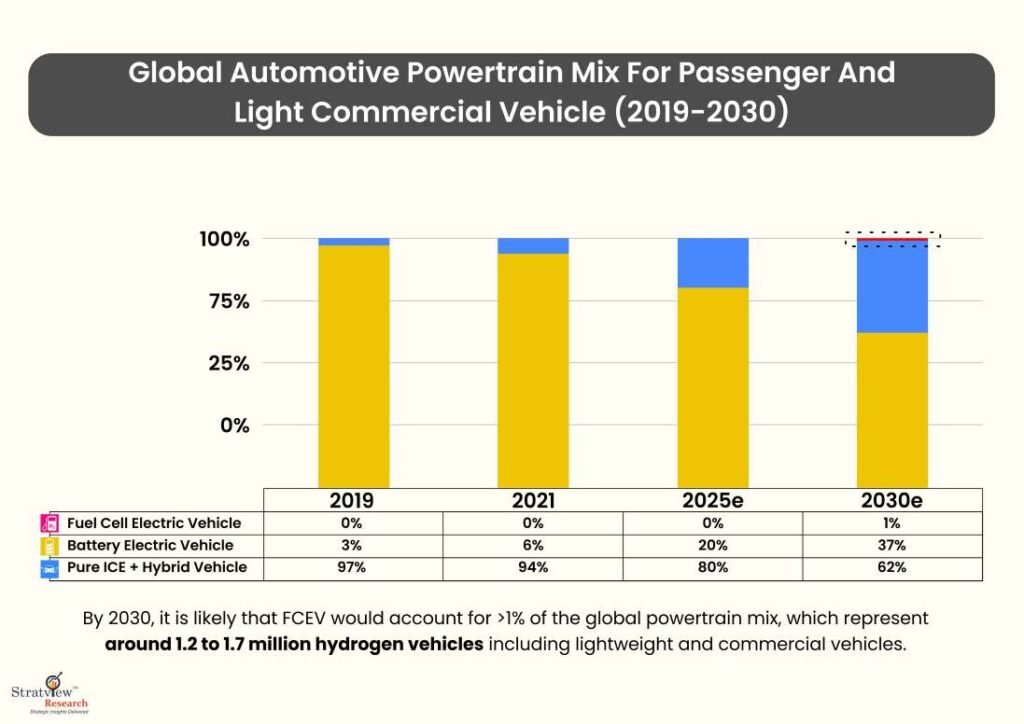

Fig.1. Global Automotive Powertrain Mix for Passenger and Light Commercial Vehicles (2019-2030)

It is expected that by 2030, FCEVs will account for >1% of the global powertrain mix, which would represent around 1.2 to 1.7 million hydrogen vehicles including lightweight and commercial vehicles, each one of which will be equipped with CCHTs for hydrogen storage.

Challenging Charging Infrastructure

Hydrogen cars are here but is the world ready to serve its fuelling needs?

The fleet size of hydrogen-propelled vehicles has been growing since its inception. One of the most significant challenges the FCEV industry faces is energy transportation from the source to the hydrogen stations. While there is already a power grid for EVs, there are yet no hydrogen distribution networks that could support a large number of FCEVs.

There were just 1,020 hydrogen refuelling stations (HRS) globally to power 72,100 FCEVs, whereas 2.7 million public EV charging points were operational worldwide to serve 20 million EVs by the year 2022.

Korea owned more than a half of all FCEVs, followed by the US, China, Japan, Germany, and others. However, HRS in China outnumbered that of Korea since China owned most of the heavy-duty fuel cell vehicle segments (trucks and buses), followed by Korea, then Japan, Germany, and the US.

This is one of the key reasons that there are more EVs getting sold than FCEVs in Europe despite the benefits FCEVs offer such as faster fuelling and longer range.

Future of CCHTs with FCEVs

It has already been mentioned that >90% of the CCHT demand originates from FCEVs or the Transportation Industry. In the coming 5-10 years, FCEVs themselves will see an escalation in demand from all the directions because what FCEVs are capable of delivering, is in perfect alignment with the vision of reduced emissions from the Automotive Industry.

The growing economies understand the difference which FCEVs can make in the coming years and hence a lot of them have already started directing their actions towards developing a supporting atmosphere for early implementation.

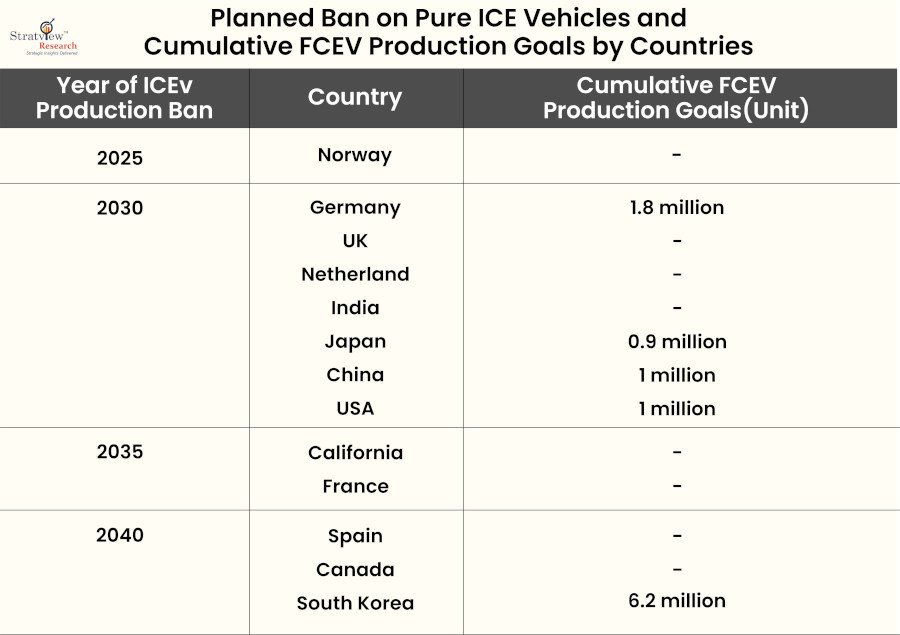

Most of the major economies have committed to strategies to boost hydrogen fuel plans and have also determined the budget they’ll be spending to reach their infrastructural goals for a more hydrogen fuel centred ecosystem. By 2040, South Korea aims to produce 6.2 million units of FCEVs, whereas by 2030 – Germany aims to manufacture 1.8 million units, China and the USA – 1 million units, and Japan to add 0.9 million FCEVs to the global fleet.

Let us look at the targets set by different nations.

Fig.2. Planned Ban on Pure ICE Vehicles and Cumulative FCEV production Goals by Different Nations

Parallelly, industry is also working into introducing innovations in CCHT designs to address the challenges they pose. Currently, Type V Pressure Vessels also exist in the market but they aren’t very popular and are not governed by any standard as of now. These are liner-less vessels made entirely out of composites and fitted with a metal boss.

Apart from the traditional cylindrical shape, the industry is exploring more volumetric efficient shapes for Pressure Vessels (PVs). And so, much of research has already begun on Toroidal Composite Overwrapped Pressure Vessels (Toroidal COPVs) as they could prove to be a viable alternative in terms of volumetric efficiency and ease of manufacturing.

This is loud and clear that the automotive industry cannot rely on one single technology to attain zero emission targets and FCEVs have undoubtedly a significant role to play in achieving those.

Along with the rise in FCEVs, CCHTs have an impressive opportunity in store and are expected witness a skyrocketing growth of over 50% during the next decade and corresponding annual sales of over USD 15 billion by 2030.

Chandana Patnaik Senior Content Writer Stratview Research